Investment opportunity management and governance

Introduction

All organisations must invest effort and capital to grow. In the private sector shareholders not only want dividends from their investments but also growth in their capital. In the public sector the community expects its tax payments to be used as efficiently as possible to protect and enhance the ‘public good’ and improve living standards.

Growth is achieved by optimising the value of assets and increasing their revenue streams. This can be achieved by process improvements, by increasing processing capability, by the acquisition of additional resources and capability and by taking on commitments and liabilities; in other words, by exposing capital to risk. If capital investments are not well managed and if investment decisions are based on poor or incomplete evaluations, this can lead to significant losses in shareholder value, diminished returns and tarnished reputations for the organisation and the executives involved.

For major capital investments, shareholders in the case of private sector projects and voters in the case of public sector projects now expect the organisations that act on their behalf to adopt rigorous processes for assembling, reviewing, selecting and evaluating investment opportunities. to ensure that they are soundly based and will generate an acceptable level of return. They also expect projects to be executed well to ensure that full value is captured.

While achievement of a predicted level of return is a key determinant of investment success, often this can only be measured some time after the investment takes place. On the other hand, much shareholder value can be destroyed when organisations fail to deliver the immediate tangible signs of an investment, such as operational plants and production activities or completion of acquisitions when and how they say they will. Investors expect management to demonstrate that they can deliver on their promises and if this does not occur, they penalise the company to reflect their lack of faith in the management team by selling the stock and devaluing the share price. In the short term, organisations that fail to deliver their growth projects on time and within budget destroy much value and lose market confidence. This not only depletes equity but can also lead to lower credit ratings and more expensive debt. This damage may be inflicted overnight but can take years to repair.

Sustained growth does not happen by accident. Shareholders expect organisations to plan a programme of growth projects, to seize opportunities when they arise and to anticipate and be prepared for changes in market conditions. This means that organisations need to create and maintain a stream of investment opportunities aligned with their potential and their need for growth. Of course, the safest projects rarely offer the largest returns and organisations have to take appropriate levels of risk to grow. As with all forms of investment, maintaining a portfolio of investment opportunities that range from low risk, low return to higher risk and higher return is required to provide options from which to build a secure strategy.

Investment opportunity management

Rather than just focussing on one project at a time and in isolation, most organisations, whatever their size and sector, need to adopt prudent processes to assemble, progress and manage a portfolio of investment opportunities. Portfolio management practices help control projects and deliver meaningful and growing value to shareholders in keeping with the organisation’s risk appetite and market.

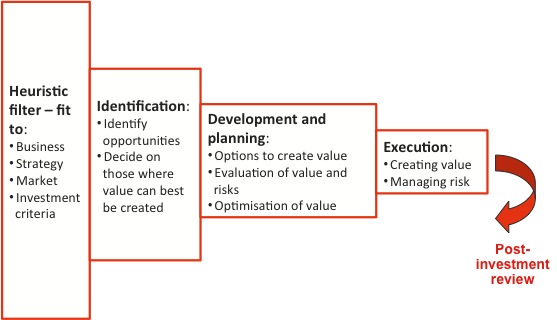

Broadleaf has helped its clients develop investment ‘funnel’ approaches like that shown in Figure 1.

Figure 1: Investment opportunity funnel

Importantly, organisations need to adopt practices that will stimulate the continual identification of investment opportunities, to ensure the funnel always keeps the development pipeline full. An investment opportunity portfolio is managed like a financial portfolio; riskier strategic investments are balanced with more conservative investments, and the mix is constantly monitored to assess which projects are still appropriate, which should be progressed and which should be abandoned or divested – in keeping with the organisation’s business strategy and market predictions.

Investment governance

While in the first phase of the investment funnel the emphasis should be on the identification of as many credible opportunities as possible, within the second phase these need to be pared down to focus on those most likely to progress to execution. It is in the second and third phases therefore that organisations need to adopt effective evaluation and governance processes to ensure that decision makers are properly informed and able to make competent decisions to ratify or decline investment opportunity submissions. Such processes are needed to both temper the natural enthusiasm of project managers and sponsors who promote their own favoured projects, while allowing good, well-planned investments to progress rapidly to fruition.

Broadleaf is now working with a number of major companies, contractors and Government agencies to enhance their investment governance processes. Our view is that all major organisations should adopt a governance framework that includes:

- An unequivocal and mandated delegation of authority or approvals framework that covers all forms of investment, expenditure and incurring of liability

- Explicit investment criteria that reflect the organisation’s strategy, business model, market and risk appetite

- A toll-gating or review point process so that as investments progress through development and planning to execution, they are periodically stopped for review and evaluation and are only allowed to proceed to the next stage if they satisfy the appropriate criteria for that toll-gate or decision point

- A hierarchy of approval and review bodies that allow decisions to be escalated in keeping with the size of the investment, the level of risks and the maturity of the submission

- Clearly defined investment evaluation methods so that all investments are assessed on a consistent, rigorous basis

- A system of uniform investment submission templates so that decision makers are always presented with a coherent and consistent set of information, in a familiar form, on which to make investment decisions

- A parallel system of competent independent review (sometimes called Independent Peer Review) that reviews investment studies and submission as well as seeking to maximise the value of the investment

- An explicit fast track procedure for high-return, low-risk investments that provides the means for rapid review and approval when there is a strategic imperative.

It is our experience that such governance frameworks can best be formulated by performance based, mandatory standards supported by guidelines. While many organisations have in the past been very prescriptive about study requirements and submission reports, we see great value in setting performance targets at each toll-gate in terms of:

- Why we should invest? – as contained in a business case, including market and strategy analysis together with an evaluation as rigorous as is appropriate for that tollgate

- What we should invest in’ – as shown in a design, to the level of precision that is appropriate for the toll-gate proposed

- How we should invest and achieve value? – as shown in a Project Execution Plan (PEP) for the next stage of the study and also for the execution of the investment.

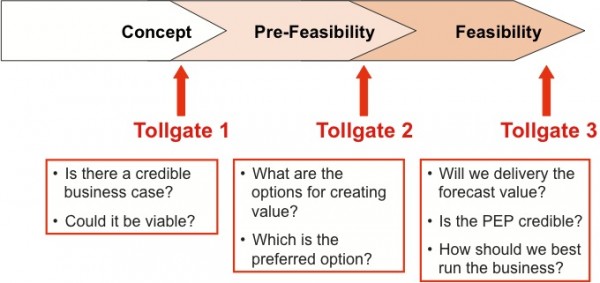

Figure 2 shows the conceptual model for such a framework. The detail must be customised to each organisation and the nature and scale of its investments to ensure that it is relevant and efficient.

Figure 2: Investment governance framework

The investment decision criteria commonly used at each tollgate are shown in Figure 3.

Figure 3: Decision criteria at each tollgate

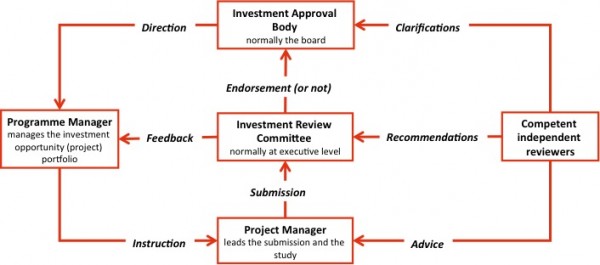

To manage the toll-gating process efficiently, to coordinate investment opportunities and to ensure consistent decision making it is normal to establish a hierarchy of roles and responsibilities that are consistent with the organisation’s approvals framework. A general arrangement for these is shown in Figure 4.

Figure 4: Roles for investment governance

Figure 4 applies to private sector organisations, but corresponding arrangements are also appropriate for the public sector. Governments in many jurisdictions have established similar governance processes, with independent reviews, to achieve the same kinds of objectives.

Broadleaf’s services

Broadleaf has helped many clients in all aspects of investment management, evaluation and governance. Our practical experience base is unique and our many service offerings include:

- Development of an entire investment management and governance framework

- Development of investment evaluation methods and criteria

- Membership of competent independent peer review teams

- Independent evaluation of review processes

- Project management

- Investment strategic option analysis

- Investment decision and real options studies

- Project risk assessment and project execution risk management

- Project return, capital and schedule quantitative risk analysis

- Post-execution and post-investment reviews

- Project audit and project auditor training

- Project risk management training

- Training and mentoring in all these topics.