Relationship between internal audit and risk management

This note addresses the relationship between internal audit and risk management functions in organisations. For many years, audit functions have used information about risk, quite properly, as one of the core inputs to audit planning. For organisations without an effective enterprise risk management (ERM) function, or one in its early stages of development, this has meant that internal audit have been forced to undertake their own risk assessments; and in many circumstances internal audit have done their own assessments anyway as a check on risk management or to assert their independence. In addition, internal audit also have to audit risk management frameworks, to provide assurance to Boards and senior management about their adequacy and effectiveness. This is a requirement of the IIA Professional Practices Standards. It is also one way that Boards can satisfy the requirements of Principle 7.2 of the ASX Corporate Governance requirements.

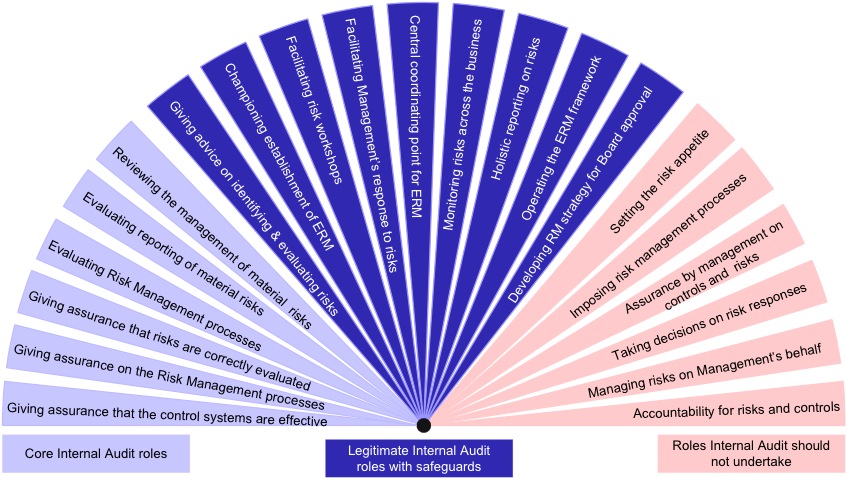

Figure 1 below, reproduced from the Standards Australia and Institute of Internal Auditors handbook HB 158-2010 Delivering assurance based on ISO 31000:2009 Risk management, illustrates a current view of the roles of internal audit and risk management. The dark-blue section in the middle of the fan is often the area of contention. Many internal auditors, and the firms who provide internal audit services on an out-sourced basis, would like to preserve the ‘consulting’ activities within their own domains.

Figure 1: Internal audit and risk management roles

Note: This diagram is taken from HB 158-2010 Delivering assurance based on ISO 31000:2009 Risk management, and is itself based on a diagram in a position statement released by the Institute of Internal Auditors – UK and Ireland in September 2004 on The Role of Internal Audit in Enterprise-wide Risk Management.

Broadleaf’s view is that the tasks in the dark-blue section of the fan should be separated from internal audit. Within most organisations there is a clear conflict of interest between internal audit and risk management in these areas. Some of the specific roles and activities that may lead to conflicts of interest are noted in Table 1.

|

Risk management |

Internal audit |

|---|---|

|

Develop the risk management framework |

Audit the adequacy and effectiveness of the risk management framework |

|

Implement the risk management framework |

Audit implementation of the risk management framework |

|

Advise management on integration of risk management into business operations and their roles in making it work |

Audit management’s commitment to risk management and the take up of their roles |

|

Advise on the allocation of accountability for risks, controls and tasks |

Audit whether accountable managers fulfil those roles and are capable |

|

Advise management and the Board on the interpretation of risk management information |

Provide independent assurance of the risk management information submitted to the Board |

|

Provide appropriate risk management status and performance information to the Board Audit and Risk Committee |

Provide an independent view on the credibility and reliability of the risk management information submitted to the Board Audit and Risk Committee |

|

Act as an advisor and mentor to management on risk management matters |

Act as an independent reviewer to provide assurance on management’s capability and performance in risk management |

Having the internal audit and risk management functions report to one manager who then, presumably, presents both sets of reports and represents both functions to the Board or a Board Audit and Risk Committee is very difficult. While internal audit and risk management have to work together, we believe it is essential that they report to separate senior managers, for clear governance purposes and to ensure that neither role is compromised. Those Chief Risk Officers who must balance internal audit, risk management and compliance portfolios often struggle with this in practice.

Apart from governance matters of the kind discussed above, there are clear management and cultural reasons for separating internal audit and risk management. Risk management is a line management function – line managers are the people ultimately responsible for delivering business outcomes, and they are responsible for managing the risks in their areas of the organisation. Having risk management separated from the line and located in a central, compliance-related area sends mixed messages to the organisation. In our view it is far better to ensure a distinct separation of internal audit and risk management, with the central risk management team having custodianship of the overall risk management framework, process and data base, but line managers having clear responsibility for risk management. The risk management function can then act as a trainer and mentor to management, to support them in their role.

While separation is important, it is vital that the risk management process generates appropriate information for internal audit to allow the development of assurance plans and timetables, including the Internal Audit Plan. Such information should include registers of the organisation’s risks, the associated controls, management’s assessment of the effectiveness of those controls, the consequences and likelihoods of each risk arising with the controls in their current state of effectiveness, and the potential exposure the organisation might face from each risk were the controls to fail completely.

Internal audit are also interested in risk treatment plans that represent management’s commitment to respond to the current level of risk. They should review the integrity of the methodology that generated the actions in those plans and track progress in completing the actions. Internal audit are also concerned with the quality and effectiveness of line management review of controls and risks through the application of methods such as control self assessment.