Valuing carbon in a plantation investment

Summary

A forestry company sought to highlight and compare the risk profiles of the market returns from sequestered carbon and timber arising from a typical first-rotation softwood plantation investment. It wished to examine the merits and opportunities of splitting or retaining single ownership of the products. We produced a model to compare the net present values (NPVs) and internal rates of return (IRRs) of future cash flows associated with carbon and timber (sawlog, pulp & biomass). The model highlighted uncertainties in the market values of the products and allowed them to be compared over a 33-year rotation.

Cash flow model

Model inputs

We constructed a financial risk model based on discounted annual cash flows over a 33-year horizon. It was built in Excel, with @Risk to model uncertainty.

The main inputs to the model are summarised in Table 1.

|

Model component |

Detail |

|---|---|

|

Land and forest costs |

Capital costs of suitable cleared land Capital costs of plantation establishment and management on predominantly cleared land Recurring annual cost of management |

|

Timber yields |

Pulp log yield Timing of saleable pulp log yield Yields for small, medium and large sawlogs Timing of saleable yields for small, medium and large sawlogs Biomass yield Timing of saleable biomass |

|

Timber prices |

Pulp log price Prices for small, medium and large sawlogs Biomass price |

|

Carbon costs |

Capital costs associated with the registration of carbon in a trading scheme Recurring costs for monitoring, reporting and auditing the carbon project |

|

Carbon yields |

Saleable carbon yield (annual carbon sequestration rate) Timing of saleable carbon yield |

|

Carbon prices |

Carbon price in $/tonne of CO2-equivalent |

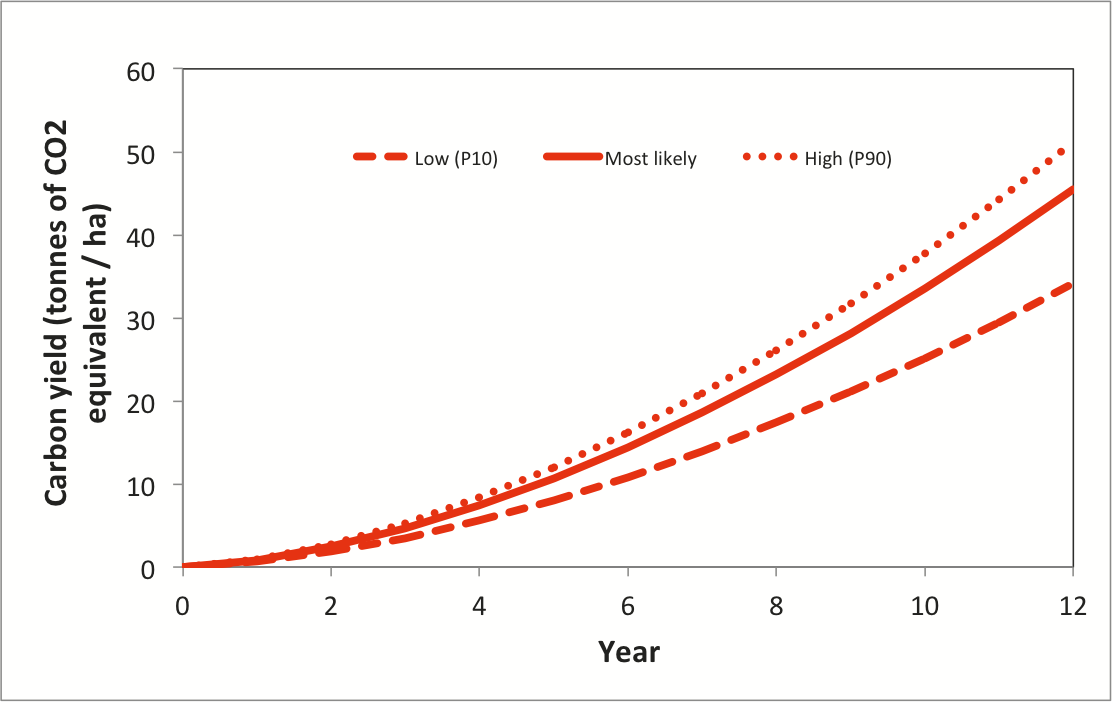

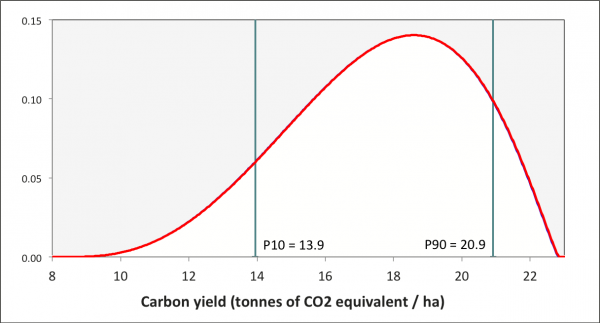

Forestry and marketing specialists in the company estimated sources of uncertainty in the components of the model in Table 1 in the form of distributions. For example, Figure 1 shows trends of the low (P10), most likely, and high (P90) values for projected carbon yield for the first few years of the life of the plantation. In any year, the carbon yield was defined in terms of a Pert distribution with the indicated values as parameters (Figure 2). Table 2 shows other selected sources of uncertainty that were taken into account.

Figure 1: Uncertainty in carbon yield

Figure 2: Pert distribution of carbon yield in year 7

|

Sources of uncertainty |

Examples |

|---|---|

|

External drivers |

Environmental factors such as drought, fire, hail, frost, snow, wind, pests and diseases Terrain characteristics Plantation yield improvements through tree breeding and mechanical utilisation Technological advances that affect the price of carbon |

|

Government decisions |

The timing of introduction of a carbon price system Change in emission reduction targets |

Model outcomes

The main outputs from the model were:

- Yields and returns for timber products through time

- Yields and returns for carbon through time

- Combined yields and returns for timber products and carbon through time.

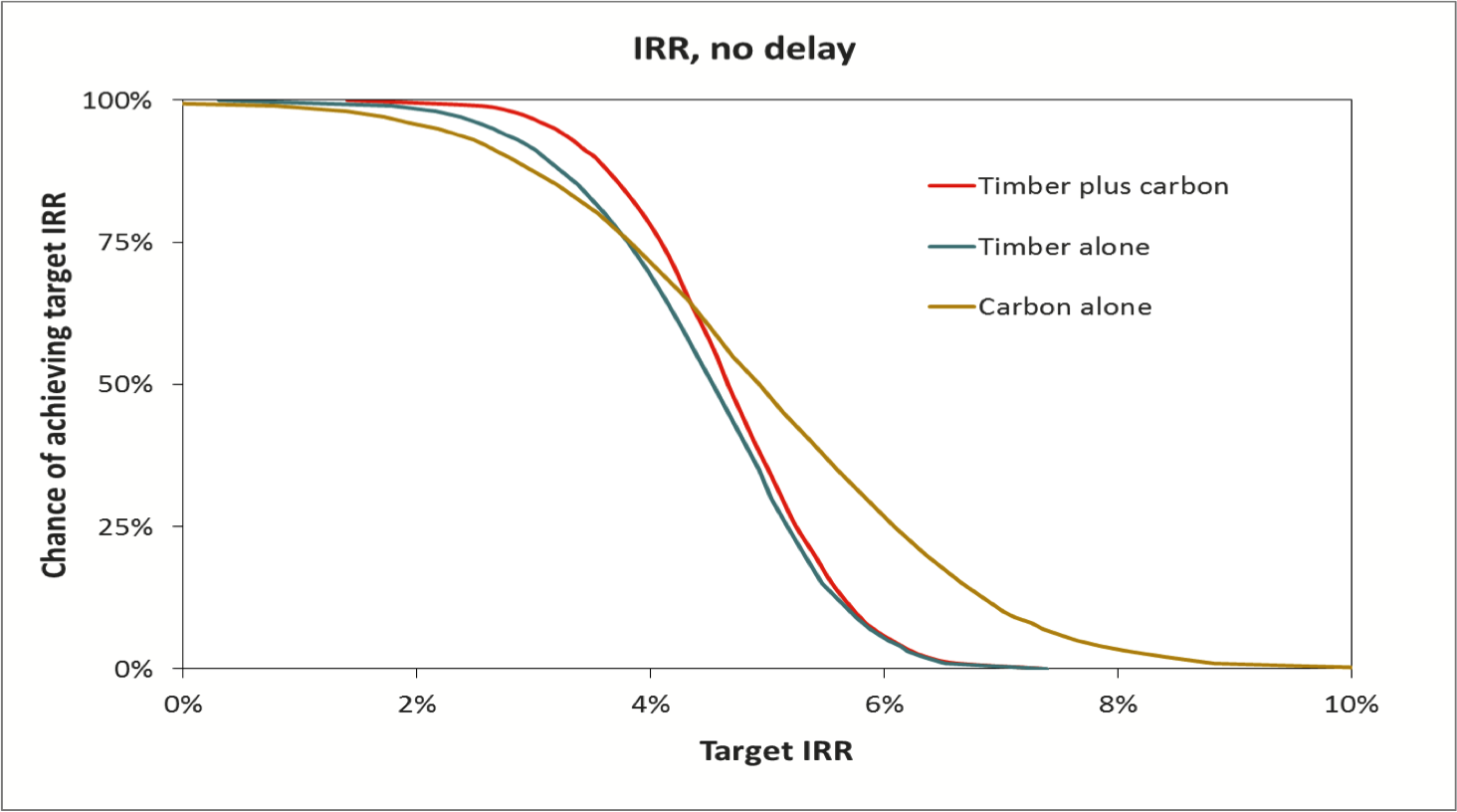

Figure 3 shows the IRR for the timber component of the investment, the carbon component and timber and carbon components combined, if the investment were made in the base year. The flatter slope on the curve for carbon indicated there was more uncertainty in the return on carbon than in the return on timber: the company had a sound understanding of forest growth and yield and it was fairly confident about the price of timber products, but it was far less confident about the future price of carbon.

Figure 3: Distribution of return with investment now

Figure 4 shows the IRRs if the investment were delayed for five years beyond the base year. The carbon component of the return now appeared far more attractive than the timber component. There was a simple reason for this: the carbon price was expected to rise in the future, whereas the revenue from saw logs was expected to fall slightly in real terms.

Figure 4: Distribution of return, delayed investment

Lessons

The evaluation model in this case used a relatively simple discounted cash flow structure. Uncertainty in the main input parameters was included in the form of distributions, and the model generated outcomes in the form of distributions. The simple structure was quite adequate to demonstrate the relative values of the carbon and timber components of the investment to the main decision makers.

The simple structure allowed different carbon price scenarios to be examined, initially using sensitivity analyses within the original model, and later with different and more specific assumptions about how carbon sequestration might be treated within the rules of a carbon market.

- Client:

- Forestry company

- Sector:

- Climate change

- Agriculture, biosecurity and the environment

- Energy

- Services included:

- Quantitative modelling