How much is a forest worth?

Overview

A public sector forestry business was contemplating asking private sector organisations to invest in new plantations, on land under its control, to produce structural grade timber.

The business intended to sell the investment rights for an up-front fee plus annual fees. It would provide forestry management services to the successful investor. Its specific objectives were to:

- Secure a long-term, reliable and cost-effective source of investment from the private sector

- Develop sustainable production over an expanded forest area

- Add value to the rural economy.

We were asked to assist in the development of financial models that would assist the business in evaluating bids from private sector proponents. In particular, we assisted in defining and modelling the returns from the Public Sector Comparator (PSC) for the reference project, which is the project as it would be undertaken by a public sector entity, using the most likely and efficient form of delivery that would satisfy the requirements. If a private sector proposal could not provide returns at least those of the reference project, then it would not be worth pursuing.

Background

All the land packages being considered had been planted with trees previously and then clear-felled. Some packages had been planted with hardwoods, others with softwoods. The proposal was concerned with second-rotation planting, generally of the same species as the first rotation. The rotation length was anticipated to be from 25 to 30 years or more.

After clear felling, a plantation passes through several phases. Table 1 outlines the phases, the products and the expected revenues. Maintenance services and infill planting continue throughout the life of the plantation.

|

Period |

Activity |

|---|---|

|

0-2 years |

Initial land preparation and planting |

|

13-14 years |

First thinning (T1): primarily used for pulp; less than 10% of total revenue |

|

20-21 years |

Second thinning (T2): primarily timber, some pulp; 25% of total revenue |

|

27-30 years |

Clear fell: final harvest of mature trees; 65% of total revenue |

The reference project

A reference project is used as the basis for evaluating private sector bids in most public private partnerships (PPPs) or private funding initiatives (PFIs). In this case the reference project was the business-as-usual approach for the public sector forestry business. This involved:

- Borrowing funds from Government to undertake the establishment and management of the plantation

- Producing and selling timber products at the best market price

- Returning funds to Government by means of dividends and interest on borrowings.

In the circumstances here, the reference project was different from the kind commonly found in PPPs.

- The asset was not standard infrastructure to be built and operated by the private sector

- The assets created – forests – grow and change over time

- Many of the risks are unique and difficult to analyse

- The public sector business would be acting as a contractor in providing forest management services, so the allocation of risks would not be the same as for a PPP where Government had no involvement.

The PSC was based on the reference project. This became the base against which private sector bids were evaluated, with allowances for:

- Competitive neutrality (benefits that would arise for the business as a result of its Government ownership, such as exemptions from some forms of charges and taxes that were not available to a bidder)

- Risk retained by Government

- Risk transferred to the private sector

- Contingent liabilities for Government.

Risk assessment

A risk assessment and allocation process was undertaken during the development of the PSC. It was conducted progressively, beginning with those risks of highest potential impact so they could be valued and incorporated in the PSC.

Initially, risks were identified and documented in a risk register, showing:

- The risk, its causes and consequences

- Its significance

- Potential treatment strategies.

Some risks would have different consequences and different treatments according to the stage in the life of the trees they affected (Table 2). The risk register and the financial risk model reflected these time-related effects.

|

Source of risk |

Period |

Effects |

|---|---|---|

|

Fire |

0-2 years |

Loss of trees; replanting required; low cost |

3-14 years |

Loss of trees; little wood recovery likely |

|

14+ years |

Salvage operations required; significant loss of wood |

|

|

Frost |

0-5 years |

Major loss of young trees; deformation of trees; replanting required |

|

Pests and diseases |

3-12 years |

Major impact on young trees; high-cost treatment required for eradication |

13+ years |

Lower-cost treatment required for eradication |

Risks were assessed against the reference project and under each investment proposal to determine whether a substantial difference existed between the options available.

- Risks that did not vary between the options were regarded as retained risks. They were not evaluated, as they would not differentiate between the options and they would not materially impact the PSC. Capital and maintenance costs were in this category, as the Government business would do the initial ground preparation and planting and provide forestry services through the life of each plantation under each commercial option.

- Risks expected to vary under different approaches were reviewed to determine whether the risk would be better transferred to the private sector or retained by the business. Revenue fell into this category, as options involved different forest and harvesting regimes, as did borrowing.

- Potentially transferable risks were further examined to determine their probabilities and financial consequences of occurrence. What the business called ‘calamities’ fell into this category, as they would be transferred to the private sector investor.

The financial risk models

We constructed a simple quantitative model of the financial risk associated with the reference project. This was a model of discounted annual cash flows over a 30-year horizon, taking into account:

- Plantation phases and tree growth (for example, related to Table 1)

- Revenues, capital costs, operating costs and variations in these factors (for example, time-related variations in Table 2 and other variations discussed further in Table 3 below)

- Costs of Government financing

- Calamities (significant risks, discussed further below).

As the proposed investment progressed and private sector involvement was sought, the cash flow model for the reference project was adjusted to generate further models that reflected specific proposals and bids by the proponents. No proponent offered a conforming bid, so flexible modelling was required.

Sources of variation

Table 3 summarises some of the main sources of variability and how they were dealt with in the financial models.

|

Source |

Discussion, treatment in the models |

|---|---|

|

Direct and indirect costs |

These would not differentiate between the reference project and an investment proposal, so variations in them were omitted from the models |

|

Interest |

Interest rate variations were included in the models, with different base interest rates appropriate for Government and private sector borrowers |

|

Revenues |

Revenue variations were driven largely by variations in market prices, incremental timber yields and yields associated with climate change |

|

Calamities |

Calamities, low probability but high consequence risks, were viewed as transferable risks that a bidder would have to treat, most commonly by insurance |

Model outcomes

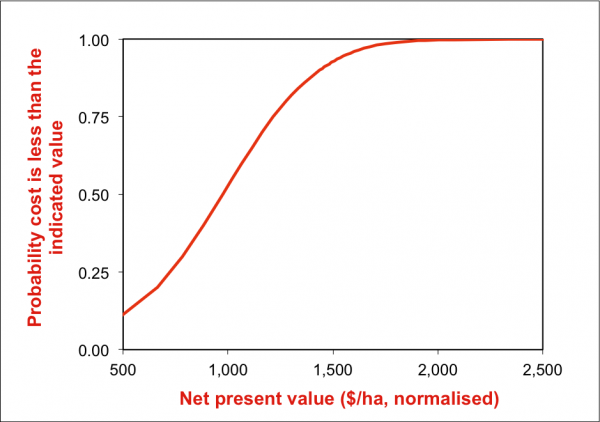

The distribution of net present value for the reference project is shown in Figure 1. This takes into account the sources of variation noted in Table 3.

Figure 1: Normalised NPV for the reference project

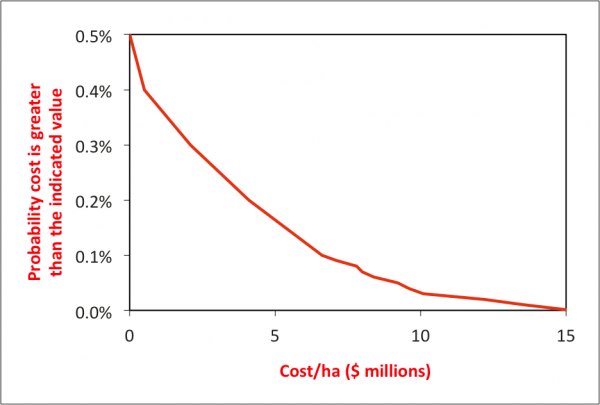

Calamities

A separate list of ‘calamities’ was prepared, largely associated with natural events like fire, frost or wind, that would have an effect on the amount or quality of timber harvested, usually by killing the trees. Generally these were events with low probabilities of occurrence, but they had potentially high consequences as they reduced the mature timber available for planned harvest. Some of them were mutually exclusive; a calamity that largely destroys the forest makes any further calamities irrelevant. The aggregate cost of calamities is illustrated in Figure 3.

Figure 3: Costs of calamities

Lessons

In an ideal world, all bidders would submit conforming responses. The formats might vary, but they would follow the rules, and non-conforming bids would be set aside. However, initial discussions indicated fairly quickly that private sector investors viewed this proposal as not standard and having high uncertainty. This meant that the financial models used for evaluation had to be structured flexibly, so that different arrangements could be examined quickly, easily and transparently. In this case no bidder lodged a bid that was fully compliant with the request!

We set out to build simple, flexible models.

- We used a cash-flow structure with only a few key revenue and expense variables for each land package. Detail was reserved for the individual land packages and their combinations.

- The focus on sources of variation that differentiated between the reference project and the proposed investment was a further factor that allowed the financial models to be simplified significantly.

Our client was pleased that we had started with simple, flexible models. It proved to be better for evaluation to have simple models that could be modified easily and allowed quick comparisons, rather than highly detailed or complex ones. As it turned out, the differences between the reference project and the investment options proposed by bidders were relatively large, so additional model detail would not have added any additional information – the preferred options were quite clear.

- Client:

- Public sector forestry company

- Sector:

- Finance

- Public sector and government business

- Climate change

- Agriculture, biosecurity and the environment

- Services included:

- Market testing and outsourcing

- Quantitative modelling