Business case for a wind farm

Summary

Broadleaf worked closely with the proponent of a wind farm development to assist in constructing a business case and an information memorandum for potential investors. Our work was particularly concerned with aspects of uncertainty in the business. This case study outlines some of the more interesting features of our work.

Background

Wind turbines convert the energy of the wind into mechanical power. In wind turbine generators, this mechanical energy is converted into electricity, which for larger units is fed directly to the grid. Wind turbines are usually grouped into wind farms that share common infrastructure such as a common connection to the electricity grid.

The central issue surrounding wind power is supply reliability. While the turbines themselves are proven and reliable, wind itself fluctuates so it cannot be relied upon as a base load power source. However, in the proper locations, wind can be an excellent source of cost effective generation into the grid.

New technologies are:

- Increasing the efficiency of harnessing wind power

- Improving the cost effectiveness, efficiency, reliability and durability of wind turbines.

Broadleaf worked with a proponent of wind energy that wanted to become a significant player in the wind power sector by developing a portfolio of wind farms. Its objectives were to:

- Generate green energy with high returns

- Deliver generating capacity in a short period

- Maximise long-term returns

- Provide safe working conditions for employees and contractors.

We worked with the proponent to establish the foundation of a business case and the material to be used in approaching potential investors. Our focus was on the uncertainty involved in such a business. Table 1 shows some of the main questions that were addressed.

|

Key question |

Topic |

Detailed topics |

|---|---|---|

|

Why have these sites been chosen? |

Weather factors |

Selection criteria; relative weighting of each criterion; elimination process; wind data reliability; comparison of weather data to existing wind farms; variability |

Physical site criteria |

Location; access by road, rail or other; proximity to power grid; ability to secure the site; local planning; environmental features; differences from current ‘accepted’ practices; size of farm (expressed as a range of number of turbines) |

|

|

How do we know this is the best value option? |

Configuration of the farm |

Number of turbines; location and layout; selection of turbines; regulatory approvals; connection to grid |

Capital costs |

Contractor; form of contract; project timeline; critical path; key elements of critical path; expenditure pattern; capital commitment compared with expenditure patterns; price risks; currency risks; independent experts and certifiers; performance and completion risks |

|

Operating costs |

Operations costs; maintenance costs; fixed and variable components; equipment reliability |

|

Sustaining capital |

Assessment of amount required (annual provision, basis, assumptions); control; custody; usage |

|

|

What will be the operating capacity of the wind farm (in MW)? |

Physical operations |

When do the turbines operate; how much electricity is generated; is there a minimum required before transfer to the grid; how is the grid monitored and controlled; is there a need to store surplus power generated; what is the operating capacity of the turbines; at what level do they operate (% of capacity)? |

|

Can we sell the power we generate? |

Market dynamics |

Demand for green energy; political influences; pricing structure |

Primary market |

Contract basis; term; revenue calculation; discount to spot market rate; ‘green credits’ |

|

Secondary market |

Spot market; market volatility; depth of spot market |

|

Alternative markets |

Industry; retail; vertically integrated ‘green’ supplier |

Qualitative risk assessment

At an early stage of our involvement, we conducted an initial qualitative risk assessment. We developed initial lists of things that might be important from documents and web sites using a range of sources available at that time, including the Australian CSIRO, the Danish Wind Industry Association, the annual reports of IEA Wind and others. We grouped them in categories (Table 2), and used them as a starting point for more extensive brainstorming.

|

Item |

Element |

Description |

|---|---|---|

|

1 |

Site and wind resource |

Location, wind resource, seasonal variability, daily variability, connection, selection process, information |

|

2 |

Land |

Availability, wind rights, competition, accessibility, construction, local resources, geotechnology |

|

3 |

Approvals |

Environmental, council, government, landowners |

|

4 |

Engineering |

Turbine numbers and type, analysis and selection process |

|

5 |

Plant |

Technology considerations, performance, availability, suitability, selection |

|

7 |

Grid connection |

Connection, easement, power purchase agreement performance, grid suitability, selection |

|

8 |

Resources |

Local resources, contractors, services, engineering, consultants |

|

9 |

Suppliers |

Turbine suppliers |

|

10 |

Supply |

Fabrication, shipping, transport to site, site preparation, civils, erection, commissioning |

|

11 |

Operation and maintenance |

Operation, control, maintenance, availability, spares, knowledge and support |

|

12 |

Security and safety |

Site security, safety operation and installation, accident events, response, sabotage |

|

13 |

Project management |

Project management resources, processes, procurement, tendering, contracting, change management |

|

14 |

Owners |

Owners’ input and influence |

|

15 |

Compliance |

Legal, environmental, community, council, safety, contractual, image, reputation |

|

16 |

Natural perils |

Wind, rain, lightning, earthquake, flood, erosion, landslips, fires, vermin |

A selection of the high risks that we identified is shown in Table 3. The risk register that was generated formed just one of the inputs to the quantitative analysis of uncertainty that followed.

|

Number |

Risk |

|---|---|

|

1.04 |

The monitored wind data shows a large difference from the modelled data; the difference could be positive or negative |

|

3.01 |

Planning and environmental approval is not granted; for example, because of an unexpected problem like a sacred site |

|

9.03 |

Supplier delays in delivery |

|

13.01 |

Inexperience of the project management company in the specific nature of these projects results in poor project outcomes |

|

13.02 |

Bad weather delays installation and results in major difficulties: for example, the crane or contractor has to be somewhere else |

|

15.01 |

The wind farm as developed does not comply with planning requirements (e.g. due to excessive noise) leading to restricted operation of the site |

Quantitative modelling of uncertainty

Overview

Quantitative risk analysis was used to model the uncertainty in the timing and cash flow forecasts through development and into operation across a portfolio of wind farms. The model took account of uncertainty in:

- Capital and operating cost estimates

- The timing of approvals, procurement and implementation activities for each farm

- Wind energy availability at each site

- Design efficiency in tapping the available energy

- Tariffs and revenue.

Because all these sources of uncertainty would be of interest to potential investors, the modelling was used to highlight areas that would need clarification before the consortium approached the market for financing. These were valuable for guiding the early activity of the development team.

The cash flow uncertainty model was used to optimise the design and project implementation. The aim was to ensure, as far as possible, that the risk associated with the financial targets for the business was limited and the measures required to control that risk were well understood and implemented properly.

Planning and forecasting covered all aspects of each wind farm, including securing sites and connection agreements, power purchase agreements (PPAs), procurement, contract and site management and overall project management. The estimates of schedule were continually refined and analysed to identify and accelerate critical path activities. The aim was to minimise the time taken between project start up and commencement of power generation at the first site to be developed.

The project cost and time planning model was integrated with a financial model to generate:

- Project rates of return

- Business valuations

- Pre-tax and post-tax returns

- Accounting cash flows and financial statements

- Financial ratio analyses.

The financial model could be tailored to generate the key parameters required by either equity investors or debt providers. It was capable of producing sensitivity analyses on key variables such as wind resource, capital and operating costs, gearing, debt term and rates of return.

Model structure

There were two kinds of components in the cash flow model:

- Primary items that represented expenditure and revenue and provided the basis for estimating the financial performance of the business (Table 4)

- Values derived from the primary items that were used to evaluate the business more broadly (Table 5).

|

Item |

Component |

Items included |

|---|---|---|

|

1 |

Start up, site identification and development |

Proponents’ initial costs; prospecting for a site; securing the right to exploit it; obtaining necessary planning, environmental and other approvals; engineering design of the plant; construction and implementation planning |

|

2 |

Sales contract and connection |

Negotiating a sale agreement; obtaining permission to connect to the grid; designing, procuring the material for and implementing a connection |

|

3 |

Implementation |

Project management; tendering; purchasing and delivery of equipment; installation; commissioning |

|

4 |

Operation |

Site leasing; plant operating costs; spares and maintenance; business management costs; revenue |

|

5 |

Finance, interest and tax |

Net cash flow and funding requirements derived from the preceding four sets of items; depreciation of the capital; tax on the net profit after depreciation; debt funding and interest; equity funding and dividends |

|

Item |

Component |

Items included |

|---|---|---|

|

1 |

Source and application of funds |

Debt; equity; proponents’ contributions; capital costs; operating costs; revenue; interest and dividends; tax |

|

2 |

Shareholder value analysis |

Free operating cash flow; dividends; tax on dividends; discounted shareholder cash flow |

|

3 |

Business valuation analysis |

Free operating cash flow; interest and dividends; tax; terminal value of the investment; discounted free cash flow after interest, dividends and tax |

Values for the main model components, and the assumptions underlying them, were documented carefully, so the model and its outcomes could be explained to potential investors. Table 6 shows examples of extracts from estimating worksheets. While these examples are very generic for reasons of commercial sensitivity, parts of the model contained significant technical and operational detail, quantitative estimates and ranges of uncertainty.

|

Item |

Basis for estimate |

Assumptions |

|---|---|---|

|

Depreciation |

Straight line depreciation of all capital over an assumed twenty year life from the year of expenditure |

Proponents’ costs and all management costs associated with establishing the plant are capitalised, as well as all equipment and services purchased |

|

Tax |

30% on net cash flow after interest and depreciation |

Constant tax rate over the asset life |

|

Interest on debt |

Percentage of outstanding debt on a monthly basis |

Interest charged at xx%, assumed fixed for this model and subject to sensitivity testing |

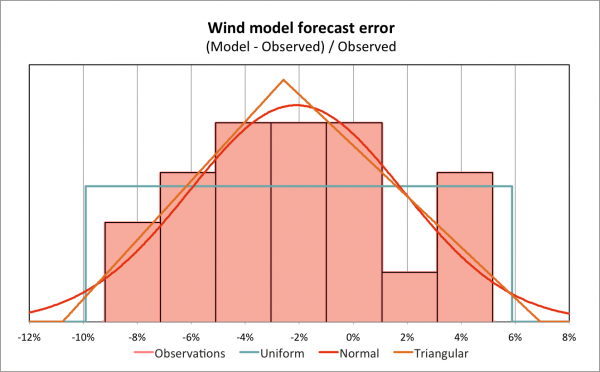

Historical data show aspects of the uncertainties involved, based on material from Steggel et al (2002). Figure 1 shows the divergence between the forecasts of mean annual wind speed from the WindScape regional wind model and the actual wind speeds observed at 21 sites using anemometers on towers. Bearing in mind the age of this example and the effort devoted to improving wind models since then, we can draw several conclusions from this graph:

- Wind models can be remarkably accurate in terms of the range of deviations from observations. Although Figure 1 is based on mean annual wind speeds, other wind characteristics like wind direction, annual power output and wind speed through time are also predicted well. Such wind models are a valuable aid in wind prospecting, selecting potential sites for wind farms.

- In the early stages of developing a wind farm, empirical data are unlikely to be available so forecasts from wind models must be used. The uncertainty in wind energy at a site, as represented by the divergence between model forecasts and observations, is large enough to be included in a quantitative risk analysis, in the absence of extended on-site observations.

- The uniform, normal and triangular distributions shown are all plausible and demonstrate similar goodness-of-fit to observations.

- Empirical data from observations on the proposed site of a wind farm are strongly recommended. The time taken to collect sufficient wind data to provide confidence and support for commercial decisions must be included in project schedules and hence in cash flow models.

Figure 1: Wind model forecasts

Lessons

Developing and documenting a business case can be an extensive, time-consuming and expensive process. While aspects of an ‘internal’ business case can be assumed as known – related to matters of corporate policy and risk appetite for example – more rigorous and transparent exposition is required for external finance providers and their clients. In addition, simple economic models of cash flows that show net present values and rates of return must be extended to show a wider, enterprise view of the business that is proposed and its after-tax implications.

Realistic modelling of uncertainty is required in either case, but model outputs may need to be explained in a different way for a wider audience that might be less familiar with the concepts of probability and distributions.

Selected references

Coppin, PA, Ayotte, KW, and Steggel, N (2003) Wind resource assessment in Australia – a planners guide. CSIRO Wind Energy Research Unit.

CSIRO Wind Energy Research Unit.

Danish Wind Industry Association.

IEA Wind, the International Energy Agency (IEA) Implementing Agreement for Co-operation in the Research, Development, and Deployment of Wind Energy Systems.

Steggel, N, Ayotte, KW, Davy, RJ, and Coppin, PA (2002). Wind prospecting with WindScape. CSIRO Wind Energy Research Unit.

Windlab, a global wind energy development company established to commercialise world leading atmospheric modelling and wind energy assessment technology developed by Australia’s premier scientific research institute, the CSIRO.

To download a copy of this case, please click here.

- Client:

- Australian energy consortium

- Sector:

- Finance

- Climate change

- Agriculture, biosecurity and the environment

- Energy